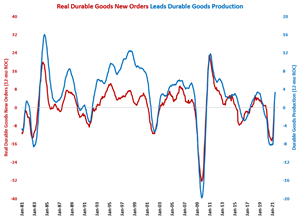

In June, durable goods capacity utilization was 74.0%. The annual change in durable goods capacity utilization grew at an accelerating rate for the second consecutive month. And, June had the fastest annual rate of growth since November 2012.

Compared with one year ago, the durable goods production index increased 12.2%, which was the fourth straight month of growth. The much stronger than normal growth is due to an easy comparison with last year when the country was just starting to exit lockdowns. The comparisons will get less easy each month.

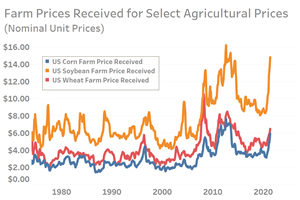

Prices received by farms for a wide range of staple crops are at multi-year and in some instances multi-decade highs. The increased revenues and associated profits will bolster agriculture machinery and equipment purchases.

Gardner Intelligence’s supplier delivery data from the Gardner Business Index (GBI) has done a commendable job of monitoring the slipping of order-to-fulfillment times for upstream supplies used in manufacturing. As delivery times have lengthened, readings have correspondingly increased and have done so well beyond anything seen in recorded history. 2021 year-to-date survey data indicate that nearly all surveyed manufacturers in June reported slowing delivery times. In fact, the last 11 months of data have reported almost an unstoppable trend of month-over-month lengthening delivery times. One would think — or at least hope— that the worst must be behind us, right? The GBI: Supplier Delivery reading has reported higher month after month readings almost consistently since July 2020.

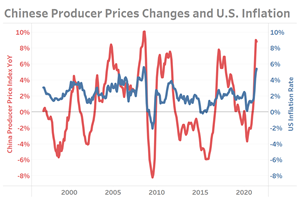

Many experts have been debating whether the current surge in inflation will be temporal or more permanent. When one moves from the theoretical realm to the reality of supply chains the picture becomes more concerning.

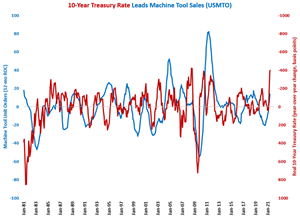

The rate of inflation increased to 5.39% in June, pushing the real 10-year Treasury rate to -3.87%. Declining real interest rates are typically a positive sign for durable goods manufacturing and capital equipment consumption.

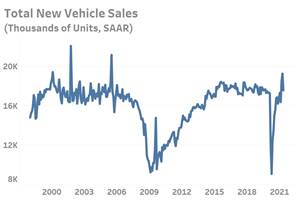

Automotive industry news during the second quarter of the year was highly concentrated around the financials of the big automakers and the improved profits they generated thanks to strong pricing despite supply chain challenges which suppressed production levels at many factories in the United States and around the world. For this reason less attention was given to monthly volumes (at seasonally adjusted annual rates, SAAR). Production constraints aside, second quarter sales volumes were impressive, led by April’s 19.2 million units reading which then gave way to a May reading of 17.5 million.

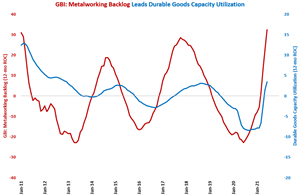

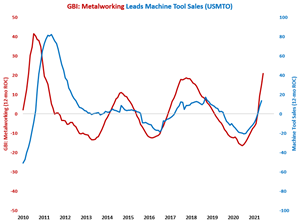

The strong growth in the metalworking industry should lead to accelerating growth in machine tool orders throughout 2021.

The Gardner Business Index moved higher in June thanks to a broad-based expansion in business activity. Quickly rising backlog and employment levels played a significant role in June’s higher reading. The month’s results also marked the first time in 2021 that Gardner’s supplier deliveries reading did not increase on the prior month. Slowing supply chains and lengthening order-to-fulfillment times correlate with rising supplier delivery readings.

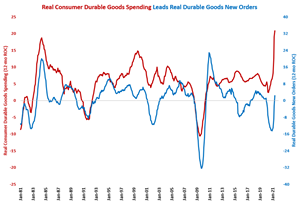

Easy comparisons with April and May have sent the month-over-month rate of growth in durable goods new orders skyrocketing. With a few months of easy comparisons and strong consumer durable goods spending, the annual rate of growth in durable goods new orders should continue to accelerate in 2021.

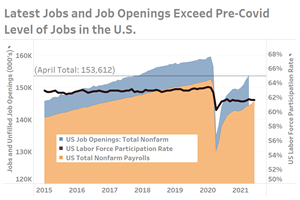

Struggling supply chains explain only part of the story behind the inability of industry to keep up with the demand for goods and services and the consequential rise in prices. As America was putting the worse of COVID behind it during the first half of 2021, a large proportion of the workforce failed to return. Just prior to the pandemic, the labor force participation rate was just over 63%. That rate then fell to 60% with the forced closure of large portions of the select industries, but then quickly rebounded to 61.7% by September 2020. In the 9 months that followed, the labor participation rate would remain virtually unchanged.

Business Activity Advances to the Second-Highest Reading in Recorded History

After moving lower during the past two months, the Gardner Business Index (GBI) rebounded to a near all-time high of 63.1.