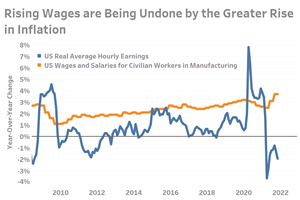

Rising prices within supply chains has already created cost control problems for manufacturers; unfortunately, there is an even more concerning “dark cloud” coming as workers see paychecks rise while their standard of living decreases. This could lead to additional rounds of wage increases.

Business Activity Expansion Slows Across Most Metrics

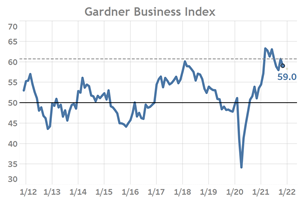

The Gardner Business Index (GBI) reported slowing expansion during November with a closing reading of 59.0.

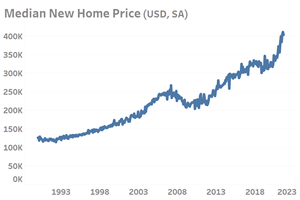

The appreciation of home prices in the 5-quarter period ending September 2021 may be the fastest in recorded history going back to 1963.

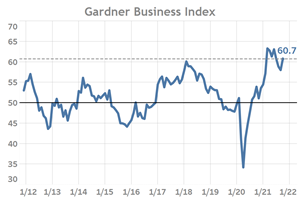

The Gardner Business Index (GBI) moved nearly 3-points higher in October to end at 60.7. Gains were widespread thanks to quickening activity in backlogs, new orders, production, and employment.

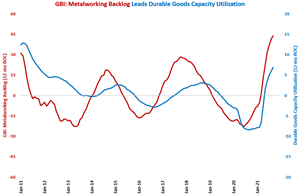

Year-over-year growth in durable goods capacity utilization was the strongest since September 2011. Every industry we track except automotive and wood/paper products was growing at an accelerating rate in September.

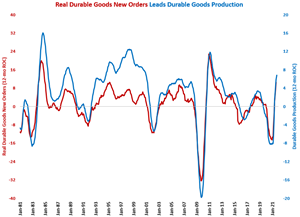

Durable goods new orders continue to grow at an accelerating rate, which would indicate that durable goods production should see accelerating growth. However, the shorter time frame rate of change in industrial production is pointing to slower annual growth is ahead.

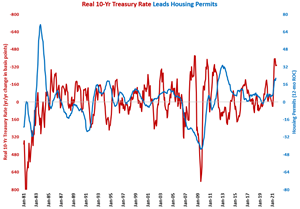

After one month of weak growth in July, housing permits grew 22.5% in August, marking the 5th month in the last six that housing permits grew more than 20%. In particular, this is a positive indicator for plastics processing production.

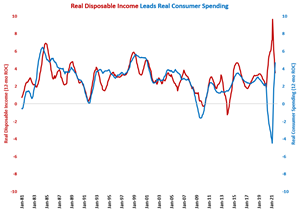

Real disposable income grew month-over-month for the first time since March. However, this was not enough to change the decelerating growth trend in the annual rate of change, which is indicating that consumer spending will hit its peak rate of growth in late 2021 or early 2022.

The month-over-month rate of growth in consumer durable goods spending grew at its slowest rate since May 2020. A significant reason for this is a 6.1% contraction in motor vehicle and parts spending as the industry is beset with supply chain disruptions.

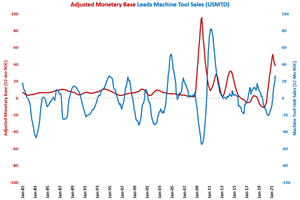

The pace of growth in the money supply has been extraordinary since the lockdowns in March 2020. August was the 21st consecutive month of month-over-month growth. And, it was the 16th in the last 17 months with growth faster than 20%. Typically, this leads to growth in capital equipment consumption.

Compared with one year ago, durable goods new orders grew 13% in August. That’s five of the last six months with double-digit growth. Given the strong growth in durable goods consumer spending, new orders should see accelerating growth for at least another three months.

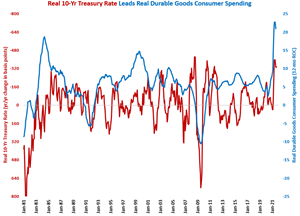

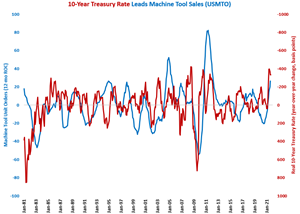

The real 10-year Treasury rate was -4.02% thanks to an increase in the rate of inflation. The extremely low real rate means that the annual change in the rate was quite negative in September, which typically leads to stronger capital equipment investment.