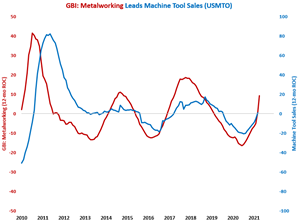

March cutting tool orders were $177.6 million, which is very close to a normal, pre-lockdown level. Starting in April, the month-over-month comparisons will get much easier, leading to rapidly accelerating growth in the rate of change. Also, the GBI: Metalworking is indicating that the level of cutting tool orders should increase throughout 2021.

The fastest rate of month-over-month growth in nearly 40 years was helped by an easy comparison with April 2020, but even with a more normal level of permits in April 2020, permits still would have grown about 33% in April.

Auto and other motor vehicle sales reached $130B in April. This is 30% above pre-pandemic levels.

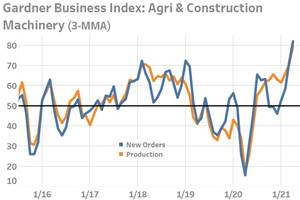

Rising prices for both new homes and agricultural products has created a surge in business activity in the construction equipment manufacturing industry.

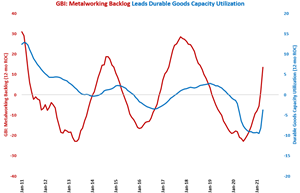

Backlogs in the GBI: Metalworking are growing at a rapidly accelerating rate. This rapidly accelerating growth rate is leading a sudden change in the rate of change in capacity utilization, which should see accelerating growth in the second half of 2021.

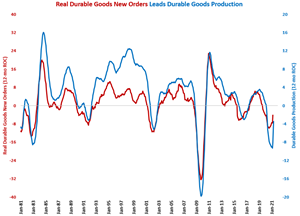

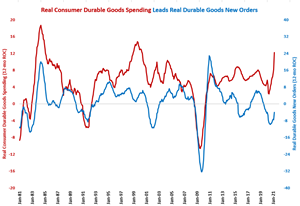

The extremely fast rate of growth in April was helped by the easy comparison with one year ago when the economy was shut down. However, April was the second straight month of accelerating growth. And, based on the trends in durable goods new orders and consumer durable goods spending, annual growth in durable goods production should accelerate in the second half of 2021.

Gardner Intelligence explains the latest manufacturing trends from its April 2021 GBI survey.

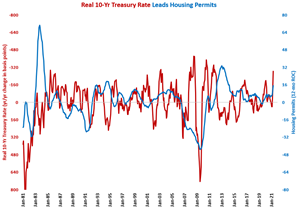

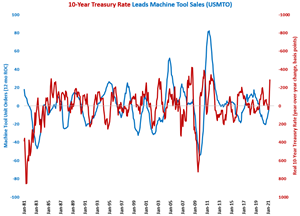

The rate of inflation increased to 4.16% in April, which was the highest rate of inflation since August 2008. As the real 10-year Treasury rate is the nominal rate minus the inflation rate, the real 10-year Treasury rate was -2.52% in March. This is very stimulative to the economy.

March’s orders were 23.4% more than one year ago, which was the fastest rate of month-over-month growth since July 2014. Numerous industries had new orders grow at double-digit rates in March.

Machine tool unit orders increased 45.1% in March compared with one year ago. While the rapid growth rate was partly due to an easy comparison with March 2020, March 2021’s 2,368 units ordered was the highest monthly unit total since March 2019. Strong growth in the GBI: Metalworking is indicating further strong growth in machine tool orders.

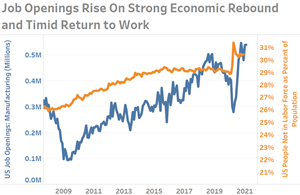

The number of unfilled manufacturing jobs during the initial months of 2021 has not been higher since the Great Recession. During most months since October 2020, the number of unfilled manufacturing jobs has exceeded 500,000. For reference, during the last business cycle of 2017-2020, the average number of unfilled manufacturing jobs was 430,000. During only two months of that cycle did unfilled openings barely reach 500,000.

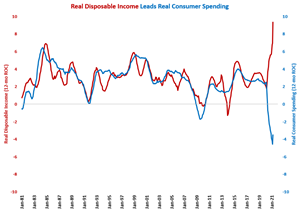

Unlike most other economic data points being reported right now, changes in real disposable income are not being affected by easy comparisons from one year ago when the economy was locked down. In fact, real disposable income in March 2020 was only 1.4% below the all-time high in disposable income. The massive increase in disposable income is purely a result of record levels of government transfer payments.