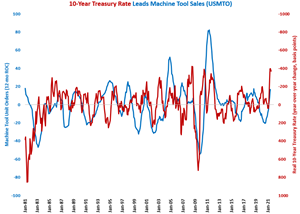

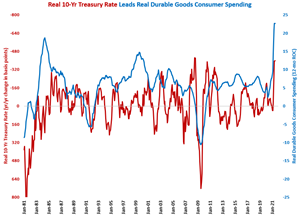

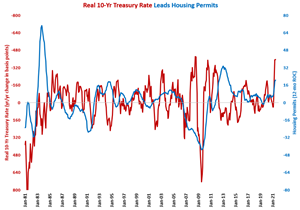

A sharp decline in the year-over-year change in real 10-year Treasury rates due to accelerating inflation indicates strong capital equipment spending for the remainder of 2021 and possibly into 2022.

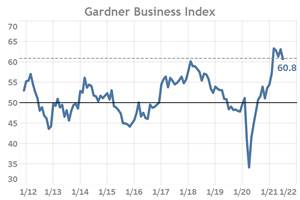

Five-Axis and Micro-machining continue to report an accelerating expansion of business activity while the broader Gardner Business Index has registered more consistent expansionary growth.

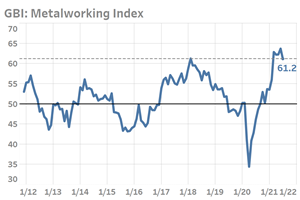

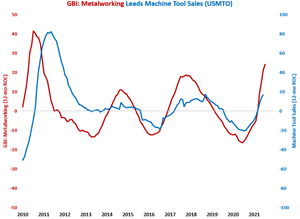

The GBI: Metalworking is growing at its fastest rate since December 2010. The rapid growth in the metalworking industry should lead to accelerating growth in machine tool orders throughout 2021.

June was the fourth straight month that new orders increased more than 27%. Of course, this very strong growth rate in June was somewhat affected by slightly lower than normal new orders in June 2020 due to the economic lockdown.

Business Activity Impacted by Slowing Expansion in New Orders

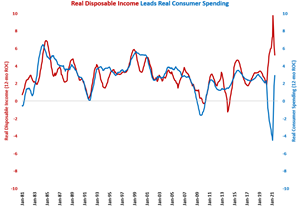

Despite an increase in nominal disposable income from one year ago, real disposable income decreased as inflation rapidly accelerated during the last year. Also, the government stimulus was not as strong this June as one year ago.

Durable goods spending in June 2021 was quite strong. In the last 13 months, month-over-month growth was more than 10% every month. And, the annual rate of growth was just 0.1% slower than the all-time high in May 2021.

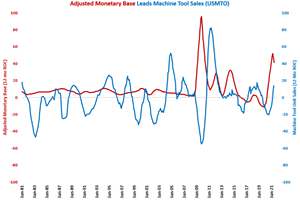

It’s staggering to realize that June 2020’s monetary base was 52.7% more than June 2019’s monetary base, and June 2021’s monetary base was 20.5 higher than June 2020’s monetary base. That’s an incredible amount of growth in just two years and is a significant contributor to the accelerating rate of inflation.

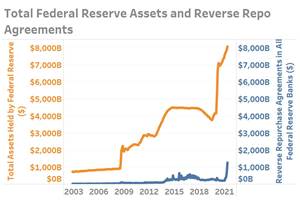

Many people talk about there being too much money in the financial system, yet justifying this argument can be difficult.

The annual rate of change in the GBI: Metalworking grew at an accelerating rate for the fourth consecutive month, indicating that the annual rate of contraction in cutting tool orders will continue to decelerate throughout 2021 as cutting tool orders continue to improve on a month by month basis.

Unlike many other economic data series, the rate of change in June 2021 was not affected by an easy comparison with June 2020. In fact, just the opposite. June 2020 was a very strong month for housing permits. Therefore, the 25.0% growth this June is a very strong rate of growth.

The rebound in the number of new manufacturing businesses since early 2020 has served as a powerful testimony to the strength and flexibility inherent to the manufacturing sector and capitalism. Not only have new business formations proven the flexibility of a free and open economy to overcome adversity, but also the ability of aspirational individuals and teams to create firms and ultimately jobs.