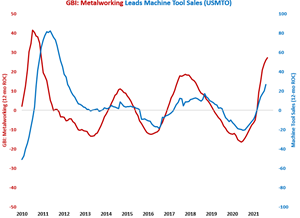

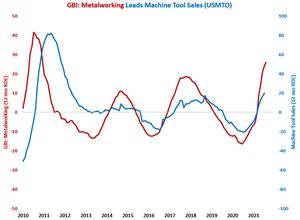

The annual rate of change in the GBI: Metalworking grew at an accelerating rate for the seventh consecutive month, indicating that the annual rate of contraction in cutting tool orders will continue to decelerate throughout 2021 as cutting tool orders continue to improve on a month-by-month basis.

The annual rate of change in the GBI: Metalworking grew 27.1% in September, which was the seventh straight month of accelerating growth. The strong growth in the metalworking industry should lead to accelerating growth in machine tool orders throughout 2021.

Business Expansion Slowed Through Third Quarter

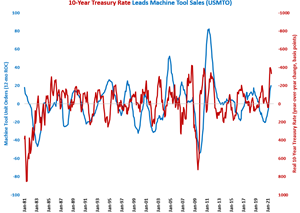

The year-over-year change in the real 10-year Treasury, now -331 basis points, was slightly less negative for the second month in a row. However, the change was still quite negative and indicating further expansion in manufacturing.

The growth of e-commerce sales and new business formations in the digital retail sector will provide an enduring support base for the packaging industry’s bright future.

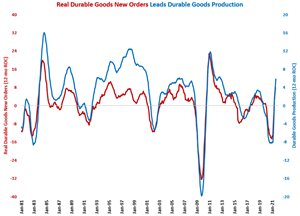

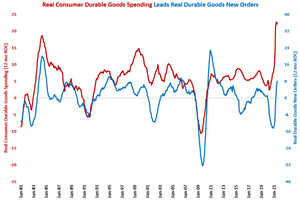

The key leading indicator of production – durable goods new orders – grew at an accelerating annual rate for the third consecutive month. Durable goods new orders are indicating that production should see accelerating growth in the second half of 2021 and possibly into 2022.

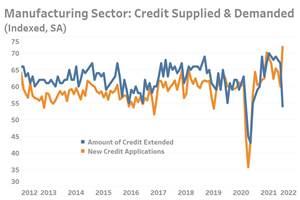

Banking data signal rising demand from companies for credit. This may support ancedotal evidence that a rising proportion of firms are struggling with limited working capital.

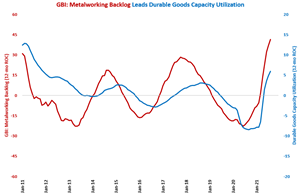

The capacity utilization in all but two of the industries tracked by Gardner Intelligence is in an accelerating growth mode (the two exceptions are growing slower). This is a positive sign for capital equipment consumption as capacity utilization leads capital spending by seven to 10 months.

Compared with one year ago, the GBI: Metalworking was 23.5% higher, which was the 13th consecutive month of growth. The strong growth in the metalworking industry should lead to accelerating growth in machine tool orders throughout 2021.

August's results indicated that persistent supply chain problems continue to have a worsening effect on production, resulting in a production 'deficit'. As a result of this deficit, manufacturers are reporting rising backlog activity and slowing hiring activity.

Annual growth in durable goods new orders should continue for another three to six months. However, it appears that consumer durable goods spending, which is a good leading indicator of new orders, may have peaked in July. Also, motor vehicle and parts, computers and electronics, and appliance new orders – all products that make heavy use of computer chips – contracted month-over-month in July.

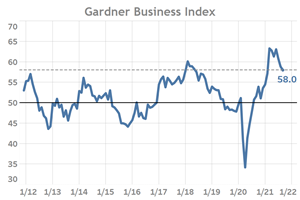

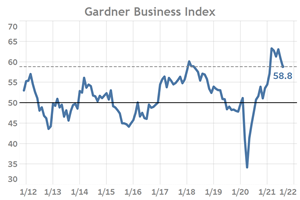

The Gardner Business Index (GBI) ended August at 58.8, marking the second consecutive month in which the overall Index moved lower.