While the nominal 10-year Treasury rate was unchanged in April, the real 10-year Treasury rate fell to its lowest rate since June 1980. The reason for this was that the rate of inflation increased to 4.99% in May, which was the highest rate of inflation since August 2008.

Gardner Intelligence provides a brief overview of the state of U.S. manufacturing for the month ending May 2021 along with actionable insights based on its proprietary data from the Gardner Business Index.

Rising production costs abroad are likely to have a direct, but smaller, impact on U.S. goods

April was the fourth straight month of month-over-month growth in durable goods new orders. Due to the strong growth in April compared with the easy comparison with one year ago, a number of industries moved to accelerating growth from decelerating contraction on an annual basis.

The private sector cannot delay to act in ways that will structurally support the economy in the long-term while the government temporarily props up the economy through debt spending. The hard truth is that delaying any efforts to build a bigger and smarter labor force now -which is within the ability of many of our readers to control- will result in severe consequences later. Even though many industry leaders are overwhelmed with work now, there is no time to delay in building tomorrow’s workforce.

Manufacturers continue to balance challenging production conditions with strong new orders activity. Delays in supplier deliveries and a lack of available new hires give some explanation for the rising levels of backlogs experienced in the year-to-date period.

The extreme rate of growth is causing significant problems in the supply chain as it is contributing to increased prices of raw materials, shipping problems, and production problems as some manufacturers are still dealing with reduced staffing.

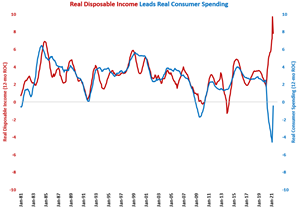

While disposable income was still historically high, the stimulus effect is starting to wear off, especially as many states have or are moving to eliminate extended unemployment benefits due to economic lockdowns. Without further stimulus to boost disposable income, it is likely that consumer spending will take a significant hit.

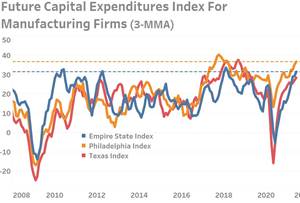

As reported by the Philadelphia Federal Reserve, the May 2021 measure of expected capital spending is at a high not experienced since 2018. This should make for a very busy second-half to 2021 for upstream manufacturers including machine tool builders and suppliers of associated tools and accessories.

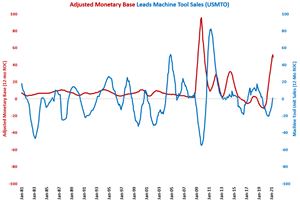

The month-over-month rate of growth in the money supply slowed for the second straight month, and the annual rate of growth slowed for the first time in 12 months. However, the annual rate of growth is the fastest ever outside of a few months during the Great Recession. This strong growth should lead to accelerating growth in capital equipment consumption for the remainder of 2021.

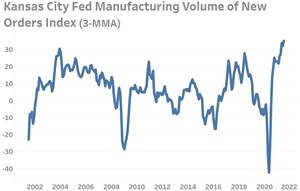

The index reading for the volume of new orders as tracked by the Kansas City Federal Reserve Bank reached 35.0 in May, besting every reading since late-2003.

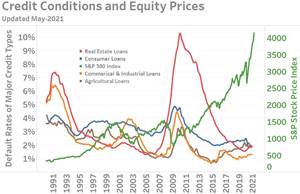

The U.S. economy’s current surge in growth is due to a multitude of factors. However, like all past economic cycles, this one too will one day end. Every downturn in the economy since the 1990’s has been preceded by eroding credit conditions. In this article Gardner provides a brief history of credit markets before each of the past recessions since the Savings and Loan Crisis of the 90’s through the Great Recession and then applies these lessons to the current economy’s conditions.