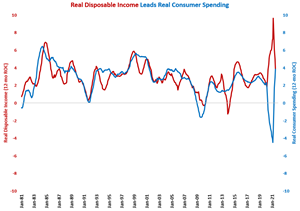

The month-over-month rate of growth in real disposable income contracted for the fourth month in a row. This led to decelerating growth in the annual rate of change, which indicates that real consumer spending will hit peak growth in the second half of 2021.

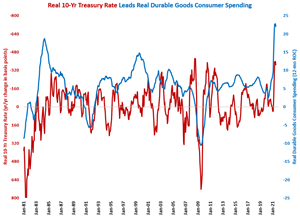

Growth in durable goods spending slowed as a result of contracting disposable income, a slight increase in the year-over-year change in the 10-year Treasury rate and fading consumer confidence. However, the most significant reason was dramatically slower growth in motor vehicle and parts spending.

Weekly data from the Association of American Railroads illustrates the diversity of supply chain problems across the continent, not just the United States.

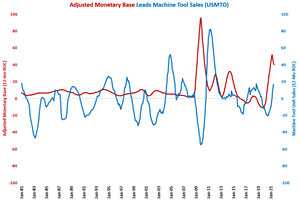

The annual rate of growth in the monetary base was rapidly accelerating through March 2021. This indicates that capital equipment consumption should see accelerating growth through March 2002, if not beyond.

The ability to implement the many available green energy solutions on a global scale greatly rests in the arms of the materials scientists and the firms supporting the production of foundational materials.

Anguish over domestic labor availability is only part of the problem facing U.S. manufacturers and ultimately product prices. Challenging labor market conditions are creating similar problems and rising production cost problems in China as well.

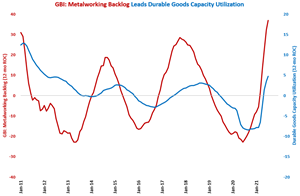

A strong recovery in metalworking, exhibited by the v-shaped recovery in the GBI: Metalworking, has led to strong growth in cutting tool orders for three straight months. Since the GBI: Metalworking leads cutting tool orders by 7-10 months, the growth in cutting tool orders should carry into 2022.

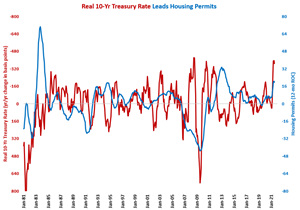

The year-over-year change in the real 10-year Treasury rate is virtually the most negative it has been since the summer of 2008. This is indicating that the slow growth in housing permits in July could be temporary.

Gardner Intelligence’s Tech Talk Session: “Using Data to Move Forward in Unprecedented Times" is available to download here.

The GBI registered slowing growth in July with a 60.8 reading, down about 2-points from June. Larger companies have reported better business conditions thus far in 2021. Conversely, firms under 50 and in particular those under 20 employees in size have been less optimistic about business conditions.

The GBI: Metalworking backlog index grew for the fifth month in a row, indicating that durable goods capacity utilization should see accelerating growth for the remainder of 2021 and into 2022.

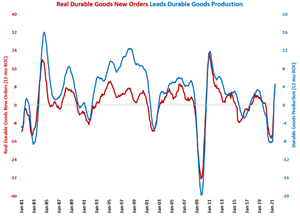

Despite falling to its lowest level since February, the durable goods production index grew for the fifth month in a row compared with one year ago. Three months of accelerating growth in the annual rate of change indicate that capital equipment consumption will accelerate into 2022.