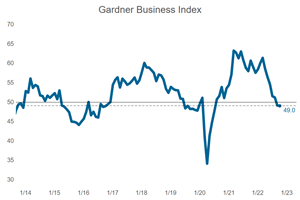

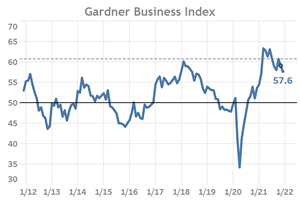

Little change from September to October as GBI hovers just under 50.

September Index drops below 50 for first time since July 2020.

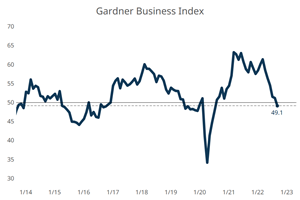

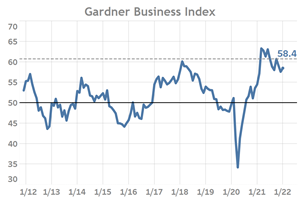

Latest Index Continues Trend of Cooling Expansion

Employment activity continues accelerated expansion as most index components decelerate.

With the exceptions of exports and supplier deliveries, 2022 has been good for trends in manufacturing activity measured as part of GBI.

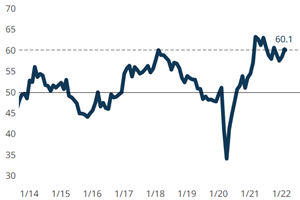

Gardner Business Index – our taking the pulse of North American durable goods manufacturing – continued to grow at an increasing rate in the second month of this year, gaining 1.7 points to close at 60.1 for February 2022.

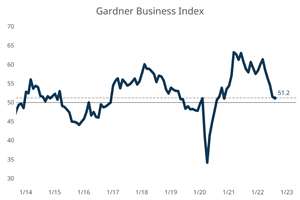

Index Reports Modest 1-Month Gain, Still 4-Points Above Year Ago Level

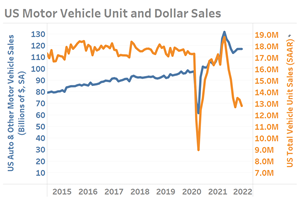

December’s U.S. motor vehicle sales fell below 13 million units for only the second time since June 2020.

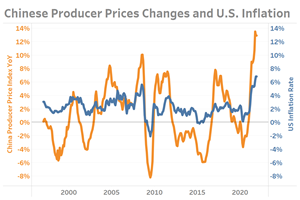

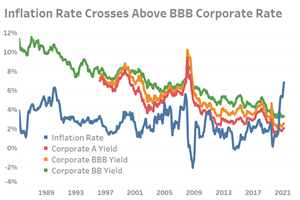

Since the early 2000’s fluctuations in Chinese producer prices have moved directionally with U.S. inflation. Recent and historical data may hold insights to near-term inflation in the U.S.

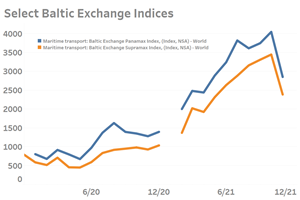

Supply chain readings during the fourth quarter of 2021 declined from both their 2021 and all-time highs. For manufacturers this will be welcomed news.

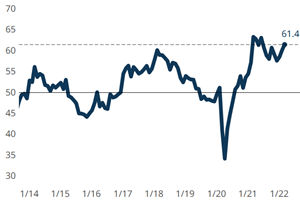

GBI Ends 2021 Slightly Better Than Where the Year Started

The latest meeting of the Federal Reserve Banks ended December 15th, 2021. In this latest meeting Bank presidents made decisive decisions designed to combat rising inflation. These actions will also ultimately result in higher borrowing costs for manufacturers.