The Gardner Business Index (GBI) has danced around 45 since June.

As far as components go, October was mostly more of the same relative to September.

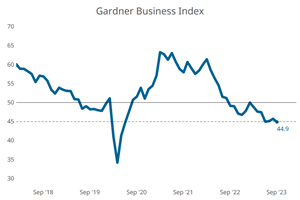

The Gardner Business Index (GBI) continued to show contracting activity, hovering around the same value for the past four months, though accelerating contraction a bit in September to land at 44.9 compared to August’s 45.7.

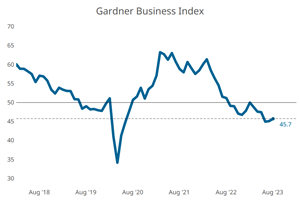

The Gardner Business Index (GBI) still showed contracting activity as it inched up again in August, landing at 45.7 compared to July’s 45.1.

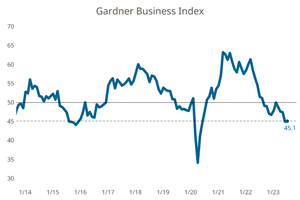

Following a relatively big drop in June, The Gardner Business Index (GBI) stayed the same in July, landing at 45.1 compared to June’s 45.0.

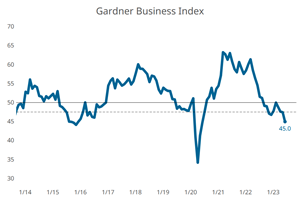

The Gardner Business Index (GBI) suffered a relatively big, -2.5, one-month drop, from 47.5 in May to 45.0 in June.

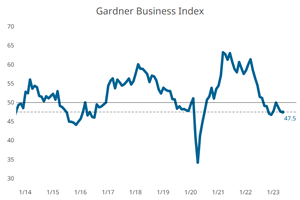

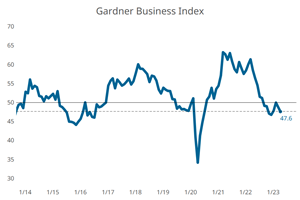

The Gardner Business Index (GBI) was nearly the same in May (47.5) as April (47.6).

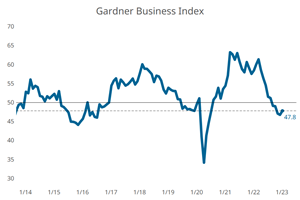

The Gardner Business Index (GBI) was down 1.3 points in April.

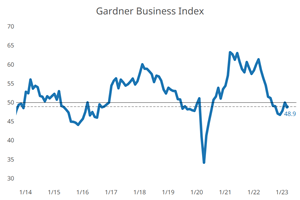

The Gardner Business Index (GBI) was down a bit in March relative to February.

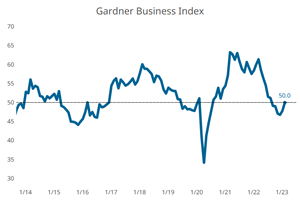

The Gardner Business Index (GBI) was ‘flat’ in February, reflecting a mix of component activity.

The Gardner Business Index (GBI) contracted a little slower in January vs. December.

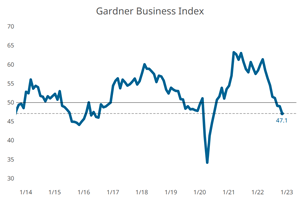

The Gardner Business Index (GBI) contracted about the same in December as November.

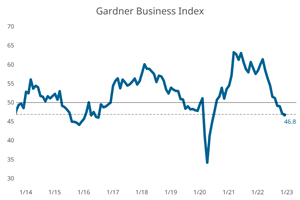

The Gardner Business Index contracted again in November, at a faster rate than that seen in October.