Discover how top manufacturers achieve industry leading quality rates and on-time delivery through data-driven benchmarking.

The Gardner Business Index (GBI) accelerates 2.2 points for December.

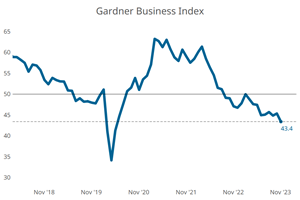

The Gardner Business Index (GBI) stabilized in July.

The Gardner Business Index (GBI) accelerated contraction in June.

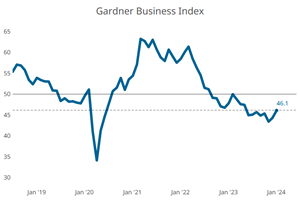

The Gardner Business Index (GBI) contracted a little faster in May.

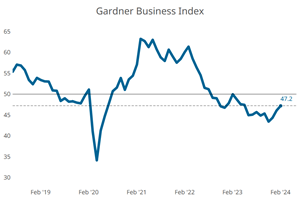

The Gardner Business Index (GBI) contracted in April to the same degree as March.

NPE2024 Insights and Opportunities: Plastics Processors Answer Suppliers Burning Questions

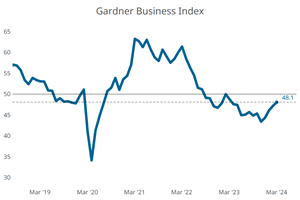

The Gardner Business Index (GBI) was up again, .9 points in March. slowing contraction each month so far this year.

The Gardner Business Index (GBI) was up 1.1 points, the highest it has been in ten months.

The Gardner Business Index (GBI) was up 1.8 points, the highest it has been in nine months.

The Gardner Business Index (GBI) was up .9 points, recovering almost one of November’s two lost points.

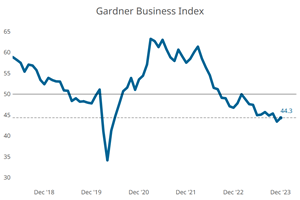

The Gardner Business Index (GBI) was down a full 2 points in November.