The month-over-month rate of change has contracted at a decelerating rate since April, indicating that the annual rate of change is about to bottom.

Gardner’s new business activity tracking tool allows subscribers to see industry changes by material types and machines used. This will provide for example glass fiber and carbon fiber fabricators the ability to see independent trends in the composites industry by material type as opposed to composites industry activity overall. This new product will also monitor metalworking shops by specific equipment utilized including five axis machines, EDMs, and grinding among others.

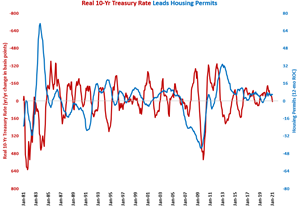

As permits are seasonal, January’s permit total was the highest for January since 2006. Short-term trends are indicating that the annual rate of growth will accelerate in the upcoming months.

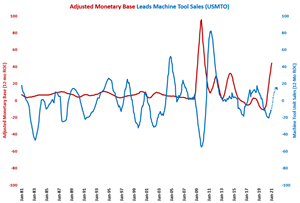

Compared with one year ago, January’s monetary base was up 52.4%, which was the fifth month in a row and seventh in the last nine months with faster than 50% growth.

The work of reinforcing and evolving manufacturing supply chains still has a long way to go in 2021. Firms which simply get their supply chain back to where it was pre-COVID will be exposed to inflating costs and the risk of lost sales opportunities.

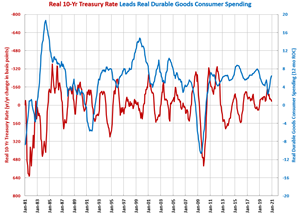

For the first time since December 2018, the year-over-year change in the real 10-year treasury rate was positive.

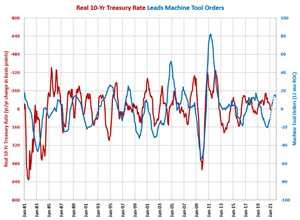

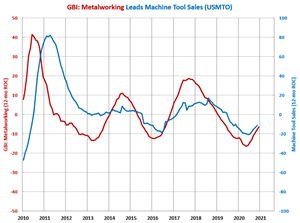

Machine tool orders reached their highest level since September 2018 (the last in-person IMTS) and their highest level outside of an IMTS month in three years.

January's manufacturing business activity data pointed to continued expansion in New Orders and Production activity.

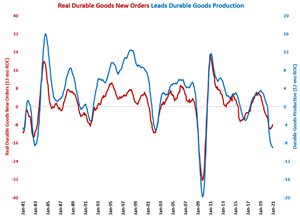

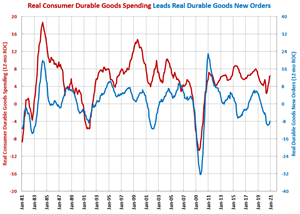

In December, durable goods new orders reached their highest total since December 2018, growing at an accelerating rate for the second month in a row.

The Gardner Business Index (GBI) increased during January thanks to expansionary readings in five of the Index’s six components. The move higher was led principally by supplier deliveries, production and new orders readings.

While total consumer spending has contracted at its fastest rate in 35 years, consumer durable goods spending grew at its fastest rate in two decades.

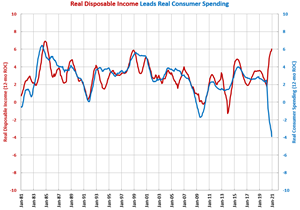

The current relationship between extreme accelerating growth in real disposable income and extreme accelerating contraction in consumer spending is unprecedented.