February industrial production contracted 3.8%. The contraction accelerated because of the winter storm in Texas and other parts of the midwest hindered production and significant supply chain disruption, particularly regarding computer chips, forced a number of manufacturers to slow or stop production.

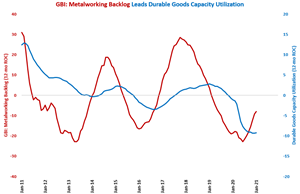

In February, durable goods capacity utilization was 71.9%, which was the lowest rate of capacity utilization since October 2019. However, it should rebound in March.

There were 117,200 housing permits filed in February 2020, which was the highest total for February since 2006.

The Gardner Business Index (GBI) notched it’s seventh consecutive month of expanding business activity. This latest expansion has been driven by strong domestic new orders -and as a result of more tepid production growth- quickly expanding backlog activity. Rising employment in the sector has also boosted overall business activity.

The real 10-year Treasury rate, which is the nominal rate minus the rate of inflation, was 0.17%. February was the first month since December 2019 that the real rate was above 0%.

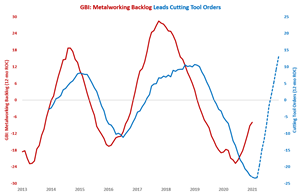

January machine tool unit orders grew 9.1%, marking the fourth month of growth in the last five months. Also, dollar orders grew for the third month in a row.

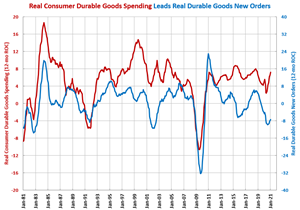

January durable goods spending got a significant boost from stimulus checks, a strong stock market, and interest rates that are still historically low.

Consumer spending continued to grow at an accelerating rate in January, which will lead to continued growth in durable new orders in the months ahead.

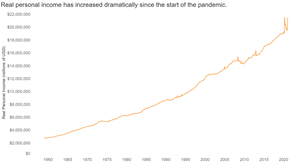

Real personal income jumped dramatically in January on the back of a new round of stimulus checks. Will an eventual reduction in stimulus mean that consumer spending will contract even faster? Perhaps not if the near record high personal savings rate falls to more recent normal levels.

Gardner Intelligence: Business Index 57.1 Business activity levels as recorded by the Gardner Business Index (GBI) expanded during February thanks to further activity gains in new orders, backlogs, and employment. Excluding export activity, all index components reported rising levels of business activity over the prior month. New orders and backlog readings for the month rose to levels last reported in mid-2018 and February’s employment activity matched readings last reported in mid-2019. The encouragement created by these gains however was tarnished by a 6-point rise in the supplier delivery reading. Rising delivery readings indicate that order-to-fulfillment times are lengthening and that manufacturers in general are struggling to obtain the upstream goods necessary to complete their orders. Removing the inflationary impact of the supplier delivery reading from the overall Index would have resulted in a March reading of 54.1, placing this series at its own 2½ year high.

The rate of capacity utilization increased for the ninth month in a row, which led to the annual rate of contraction bottoming out.

The annual rate of contraction in cutting tool orders has nearly bottomed. And, based on trends in the Gardner Business Index and macroeconomic manufacturing data, cutting tool orders should see double-digit growth by year-end.