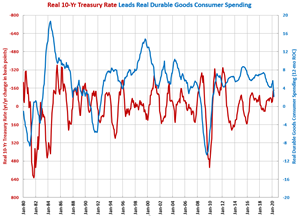

In April, real consumer durable goods spending dropped to its lowest level since September 2014.

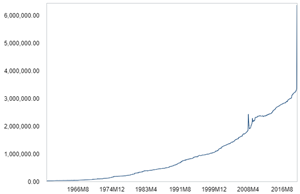

April was the highest level of real disposable income by $1.8 trillion, or roughly 12% more than the previous all-time high.

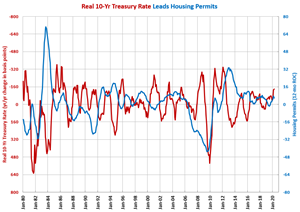

There were 96,900 housing permits filed in April 2020. Permits filed in April were down 18.4% compared with one year ago, which was the first month of contraction since June 2019.

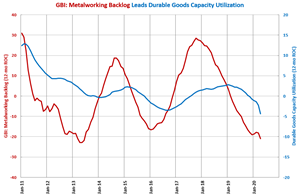

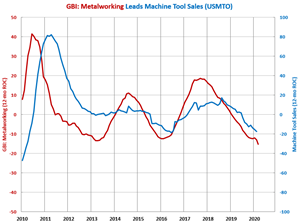

Due to the effects of the coronavirus, the GBI annual rate of contraction accelerated since March. A bottom in the annual contraction of cutting tool orders cannot be expected until seven to 10 months after a bottom in the GBI annual rate of change.

In April, durable goods capacity utilization was 55.3%, which was the lowest rate ever. Compared with one year ago, capacity utilization contracted 26.6%, which was the fastest rate of month-over-month contraction ever.

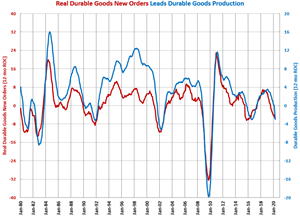

The durable goods production index fell to 79.9, contracting 26.4% month-over-month. That was the fastest rate of month-over-month contraction in the index since its inception.

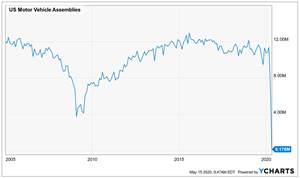

Automotive production at the end of March had fallen by one-third according to several measures. This decline was outpaced by a near 50% reduction in demand as measured by unit sales. April’s data reported a near complete shutdown of vehicle production across the country.

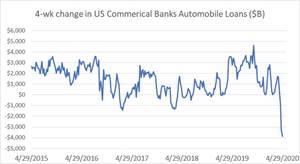

Total automobile loans in dollar terms fell every week of April, signaling weakening demand for vehicle financing.

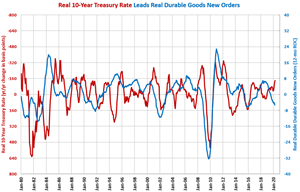

In April, the year-over-year change in the real rate was -140 basis points. The change was negative for the 16th month in a row. This was the lowest level for the year-over-change since July 2012.

Due to the COVID-19 pandemic, the GBI: Metalworking dropped sharply in March and April. This drop caused the GBI: Metalworking annual rate of contraction to accelerate once again. This will likely lead to an acceleration in the contraction of machine tool orders in March and April.

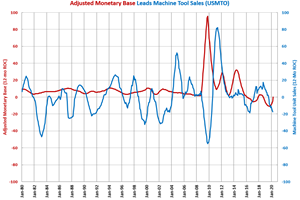

Compared with one year ago, the monetary base increased 47.4%, which was the fastest rate of month-over-month growth since October 2009. This was the fifth month in a row of month-over-month accelerating growth.

Monthly and weekly indicators of economic activity are helpful guides for monitoring changes in economic conditions. While Gardner Intelligence is pleased to share with manufacturers insights from the Gardner Business Index (GBI) each month, the WEI may be of significant help to our readers. In this article we discuss the Federal Reserve’s Weekly Economic Index (WEI).