The Gardner Business Index reported its third month of slowing contraction in July.

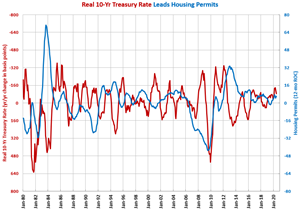

Permits filed in June were up 11.7% compared with one year ago, returning to double-digit growth after two months of contraction.

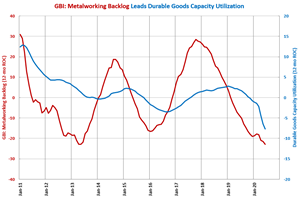

Compared with one year ago, capacity utilization contracted 15.1%, which was the second straight month that the month-over-month rate of change contracted at a slower rate.

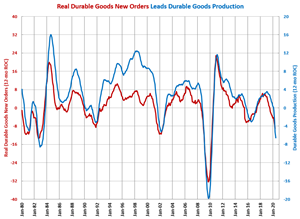

In June, the index for production of durable goods was 95.2. The index increased for the second month in a row after reaching the second-lowest level for the index since January 2010.

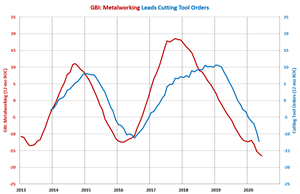

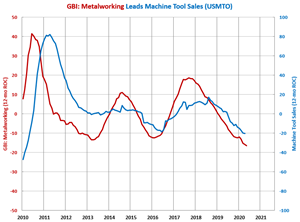

The pandemic accelerated the contraction in metalworking and extended the accelerating contraction in cutting tool orders. But, the GBI: Metalworking indicates the lows in cutting tool orders may be in the past.

Gardner Business Index data collected during June 2020 reported that new orders activity in the moldmaking and mold industry was already experiencing an initial rebound just months after COVID forced the shutdown of much of the U.S. and global economy.

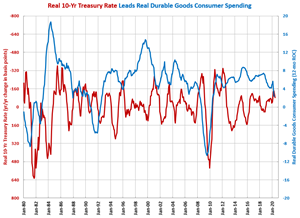

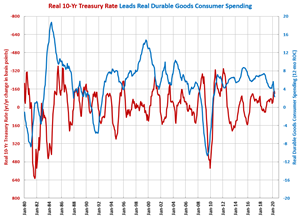

A falling change in the real 10-year Treasury rate tends to be a positive signal for durable goods manufacturing.

May’s unit orders improve slightly from April’s lowest monthly total since May 2010. However, orders for the month contracted 26.6% compared with a year ago.

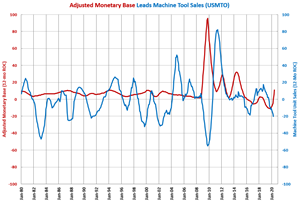

In June, the monetary base was $5.002 trillion, which was slightly lower than last month. However, compared with one year ago, June’s monetary base was up 52.7%.

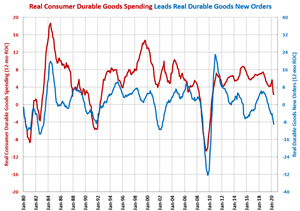

May was the second lowest total for real durable goods new orders since July 2009 and was down 22.3% from one year ago.

May consumer durable goods spending returned to pre-pandemic levels based on strength in appliance, electronics, motor vehicle and part, and pleasure boat spending.

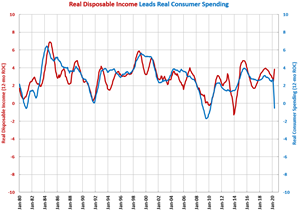

May 2020 was the second highest level of real disposable income ever. However, it was more than $800 billion lower than the income level in April